|

Getting your Trinity Audio player ready...

|

What is an interest rate derivative (IRD)?

An IRD or interest rate swap is a derivative which is a contract between 2 parties that agree to exchange interest payments between each other based on fixed and floating interest rates. IRDs are typically forward contracts where the specific term dates and prices can be customised according to the arrrangement. They are predominantly used by market participants (which can include the likes of traders, banks, borrowers and corporate treasurers) to hedge their positions or speculate market activity. However, they come with inherent market risk and exposure risk.

The most commonly used IRD is a ‘plain vanilla’ swap where fixed rate payments are exchanged for floating (or variable) rate payments based on the overnight benchmark financing rate such as SOFR (i.e. the benchmark interest rate for dollar-denominated derivatives and loans which replaced) or ESTER (Euro Short-Term Rate).

History of IRDs

Swap agreements came about from Great Britain during the 1970s to deal with fluctuations in currency rates. Originally, a swap was viewed as a back to back debt arrangement – this was because two organisations from different countries would swap debts of the currency or foreign exchange (FX) of their own countries. The purpose of this was to allow each entity to access the other country’s FX and therefore not have to pay any foreign exchange fees.

In late 1981, IRDs started to develop in the Eurobond market. This is the time when large international banks (who mostly lent out on a floating-rate basis) entered into the first IRDs to use their fixed-rate borrowing power to get cheaper floating-rate transactions. Thereafter, the first IRD entered into between non-bank counterparties, was in 1982, between Student Loan Market Association (Sallie Mae) and the ITT Financial Corp. Under this IRD, Sallie Mae paid ITT Financial Corp in floating rate payments. By 1984, there were about USD80 billion worth of swap agreements concluded. According to ISDA’s Research Note, the combined IRD notional traded across the UK, US and European Union regions amounted to US$521.5 trillion for the full 2023 year.

How an IRD works?

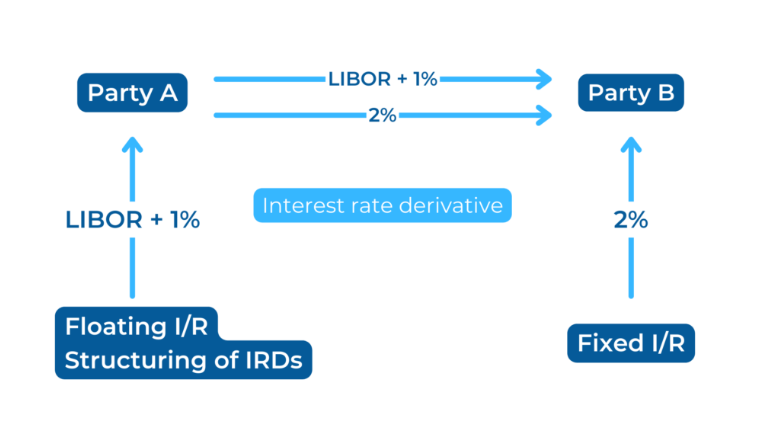

In an IRD, the interest payments are essentially the only things being exchanged – the parties do not become an owner of the other’s loans. Parties to an IRD are simply agreeing to pay the difference in the loan payments (as per their agreement) to each other.

See below diagram of how a simple IRD works:

Structuring of IRDs

There are 3 ways in which IRDs can be structured:

- Floating to fixed – this is where a party with a variable rate loan enters into a swap to get a fixed rate (as it cannot access a fixed-rate loan). The floating-rate terms on the loan are essentially identical to the swap and the two transactions off-set each other. For instance if the floating or variable interest rate rises, having the swap in place would result in a payment of an equal amount to the increase in the interest on the loan.

- Fixed to floating – this is the reverse of the above, where a party with a fixed rate loan can take advantage of variable interest rates. Their net debt payment costs would be lower if the floating swap rate they pay to their counterparty stays below the fixed rate it receives.

- Floating to floating – this is where parties enter into a swap purely to amend the maturity of the floating rate index that they pay (called a ‘basis swap’). For example, it could be swapping from a 6-month LIBOR to 12-month LIBOR, as the rate may be more attractive under the new maturity date or match a payment flow of another transaction of theirs.

Why are IRDs traded?

IRDs are an essential tool for many market participants and are used for the below purposes:

- Speculation – fixed income traders can speculate on interest rate movements since little capital is required upfront for a swap. For example, a trader could get a ‘fixed’ amount under a swap rather than investing cash or borrowed capital to buy a long-term bond or note.

- Risk management – financial institutions do a large number of transactions and the bulk of fixed and floating rate exposures would normally off-set each other, however IRDs can assist in off-setting any residual interest rate risk.

- Corporate finance – companies with floating rate debts (where loan payments are based on LIBOR for example), can enter into an IRD where they pay a fixed rate but receive a floating rate payment.

- Portfolio management – portfolio managers can adust their interest rate exposure and offset the risks of volatility in rates. Here, swaps can also be an alternative to other less liquid fixed income securities they transact in for their portfolios.

- Rate-locks on issuance of bonds – corporates that issue fixed-rate bonds can lock in current interest rates by entering a swap. During this time they can find investors for the bonds and when they sell such bonds, then exit the swap, and may be in a more favourable position according to the interest rate movement.

Reporting IRDs

The key fields to pay attention to (along with counterparty details such as the nature of the counterparty, corporate sector and LEI, ISIN & UPI identifiers) when reporting IRDs include:

- Contract type

- Asset class

- Directions of leg 1 (e.g. Payer/Receiver) and leg 2 (e.g. Receiver/Payer)

- Underlying identification and type

- Indicator of the underlying index

- Indicator of the floating rate of leg 1/2

- Floating rate day count convention of leg 1/2

- Payment frequency

- Spread, spread notation and spread currencies for leg 1 and leg 2

- Notional currency amounts of leg 1 and leg 2

- Fixed rate or coupon payment frequency period for leg 1 and leg 2

- Floating rate payment frequency period of leg 2/1

- Execution timestamp

- Effective date

- Maturity date

- Settlement date

The above may vary depending on the regulatory reporting regime that applies and on the type of interest rate swap it may be e.g. swaptions also require completion of fields related to options as well as the fields reflecting the underlying. Also, note that some of the above data fields may not be relevant to both legs of an IRD.

How can TRAction assist?

If you need assistance in understanding how to report your IRDs or want specific regulatory assistance on the updated global trade reporting rules, get in touch with us.