What is a Repurchase Agreement?

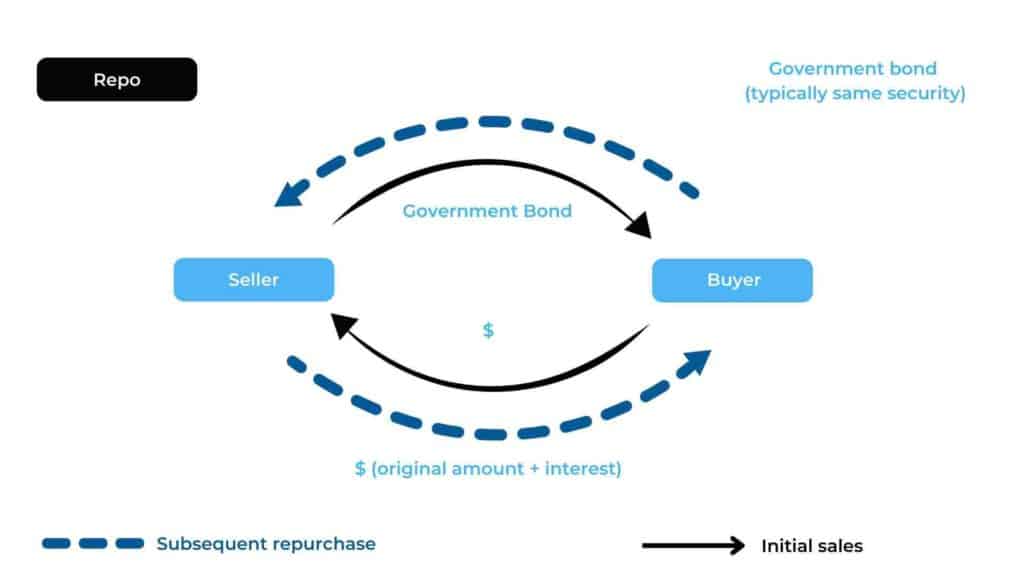

A repurchase agreement (repo) is a form of short-term secured loan where one party sells securities to another and agrees to repurchase those securities later at a higher price with the securities serving as collateral for the borrower. The difference between the securities’ initial price and their repurchase price is the interest paid on the loan, known as the repo rate. A reverse repurchase agreement (reverse repo) is the mirror of a repo transaction. In a reverse repo, one party purchases securities and agrees to sell them back for a positive return at a later date, often as soon as the next day. Most repos are overnight, though they can be longer.

Why Do Repurchase Agreements Exist?

Repurchase agreements are widely used by banks and financial institutions to regulate cash flow. Financial institutions are able to post applicable securities in order to gain liquidity in an efficient manner with low-risk and low borrowing cost. Repurchase agreements are considered low-risk investments because the securities are generally high-quality government or corporate bonds which function as collateral. The Repo market can play a key role in facilitating cash and security flow in a financial system, allowing markets to function smoothly during periods of high volatility.

The European Central Bank (ECB) allows regulated banking entities to access cash at predetermined rates which can boost asset reserves during periods of high economic stress. The ECB is able to achieve this by directly interacting with financial institutions using repo agreements.

Central Banks are also able to tighten financial conditions by entering into reverse repo agreements, which act as a drain to the excess liquidity in the system and a safe place to place cash reserves.

The Repo market can also be used to regulate money supply in the economy. For example, during periods of above-target inflation, the reserve bank lends securities to commercial banks, which helps to regulate the supply of money and therefore lending which occurs in the economy.

How are Repo Rates Determined?

Repo rates are generally competitive with the market rate for other low-risk securities. This is because the repo market is generally short-term in nature and is considered low-risk.

There are two important factors that affect the repo rates:

- the terms of the agreement (tenor and price of the collateral); and

- the quality and credit risk of securities being sold and repurchased.

Apart from the above, there are risks involved in repos, such as adverse market conditions and outstanding supply and demand of certain collateral.

How are Repurchase Agreements Reported for SFTR?

Repurchase transactions in securities, commodities or guaranteed rights relating to instruments where the guarantee is issued by a recognised exchange are all reportable under Securities Financing Transactions Regulation (SFTR).

New trades and any lifecycle events in a repo or reverse repo must be reported within one business day of the agreement. For example, when there is an extension or ad-hoc agreement to change the repurchase date of a fixed-term repo, this event will need to be reported as a modification (MODI) under the SFTR regime. All lifecycle events such as modification, collateral update (COLU) or termination (ETRM) are to be reported to a trade repository (TR) no later than the next working day. However an important point to note for repos is that a valuation update (VALU) is not required. An in-depth guide can be found in the ESMA SFTR Guidelines.

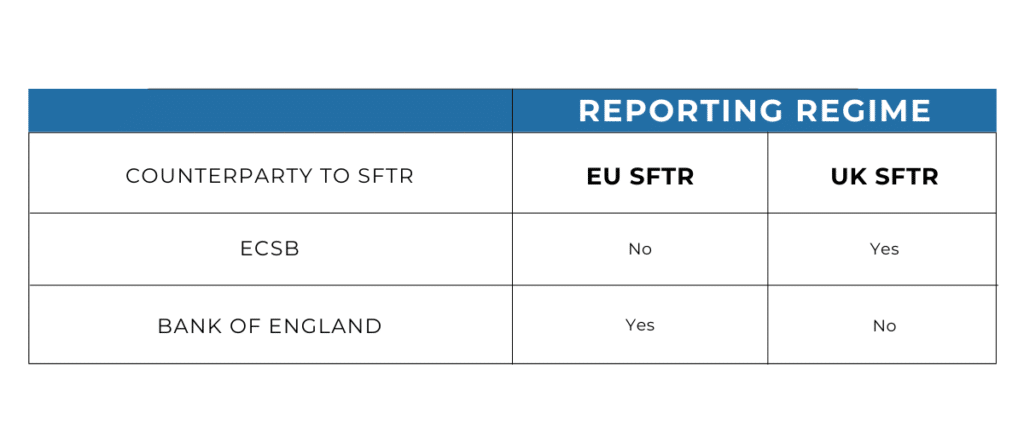

There is a distinct difference between reporting Securities Financing Transactions (“SFTs”) to EU SFTR and UK SFTR where Central Banks are party to the trade. SFTs with Central Banks which are members of the European System of Central Banks (ESCB) do not have to be reported under EU SFTR (see ESMA SFTR Article 2(3)). The ESCB consists of the European Central Bank (ECB) and the National Central Banks (NCBs) of all 27 member states of the EU.

In contrast, SFTs are reportable under UK SFTR where the counterparty is a member of the ESCB (FCA’s Handbook Notice 96) and are not reportable when the counterparty is the Bank of England.

Here are 5 important SFTR fields to be reported for repurchase agreements.

| Field | Example data | Description |

| Type of SFT | REPO | Type of SFT transaction as defined in paragraphs (7) to (10) of Article 3 of Regulation (EU) No 2365/2015. |

| Event Date | 2022-09-02 | Date on which the reportable event captured by the report took place. For example, in the case of action types ‘Valuation update’ and ‘Collateral update’, the date of such events. |

| Execution Timestamp | 2022-09-01T10:06:30Z | Date and time when the SFT was executed according to ISO 8601 date in the format and Coordinated Universal Time (UTC) time format, i.e. YYYY-MM-DDThh:mm:ssZ |

| Principal amount on value date | 20000041.32 | Cash value to be settled as of the value date of the transaction. |

| Action Type | NEWT | ‘NEWT’ – New ‘MODI’ – Modification ‘VALU’ – Valuation ‘COLU’ – Collateral update ‘EROR’ – Error ‘CORR’ – Correction ‘ETRM’ – Termination / Early Termination ‘POSC’ – Position component |

How can we help?

At TRAction, we are a specialised third party delegated reporting entity who can assist you in submitting your transactions to the designated Trade Repository.

Please contact us if you would like to know more about how to simplify your reporting.